Jul 2006

One Day Lecture at s:f:i

23. 07 06 - 23:47 - Category:Mathematics

(English Text)

The lecture will take place August 2nd at University of Lausanne. See the program of this event for details. As precourse reading you should consider Chapter 8, 9 and 10 (interest rate basics), Chapter 12 (exotic derivatives) and Chapter 15 (libor market model) of my lecture notes. These chapters are available in english and german.

Black Moleskine notebook missing

15. 07 06 - 23:16 - Category:Private

(English Text)

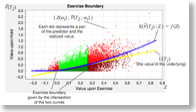

Foresight Bias

14. 07 06 - 22:45 - Category:Mathematics

(English Text)